One AI server, from the GPU at its core to the rack on the outside, sets a whole row of Taiwanese companies in motion. Within the AI supply chain, the most advanced AI compute chips are designed in the United States and memory is led by the US and South Korea — but there is one segment that is unambiguously Taiwan’s home turf: assembling all the parts into a working AI server.

This piece spells out AI server stocks. First, what an AI server is made of; then Taiwan’s division-of-labor map across system assembly, cooling, power, networking, connectors, and substrates; and finally what GB300 changed in the supply chain. This is the server-system-layer extension of the Taiwan semiconductor supply-chain gate.

What an AI Server Is Made Of

Start with one idea: today’s AI server is mostly in the form of a “full rack-scale system.”

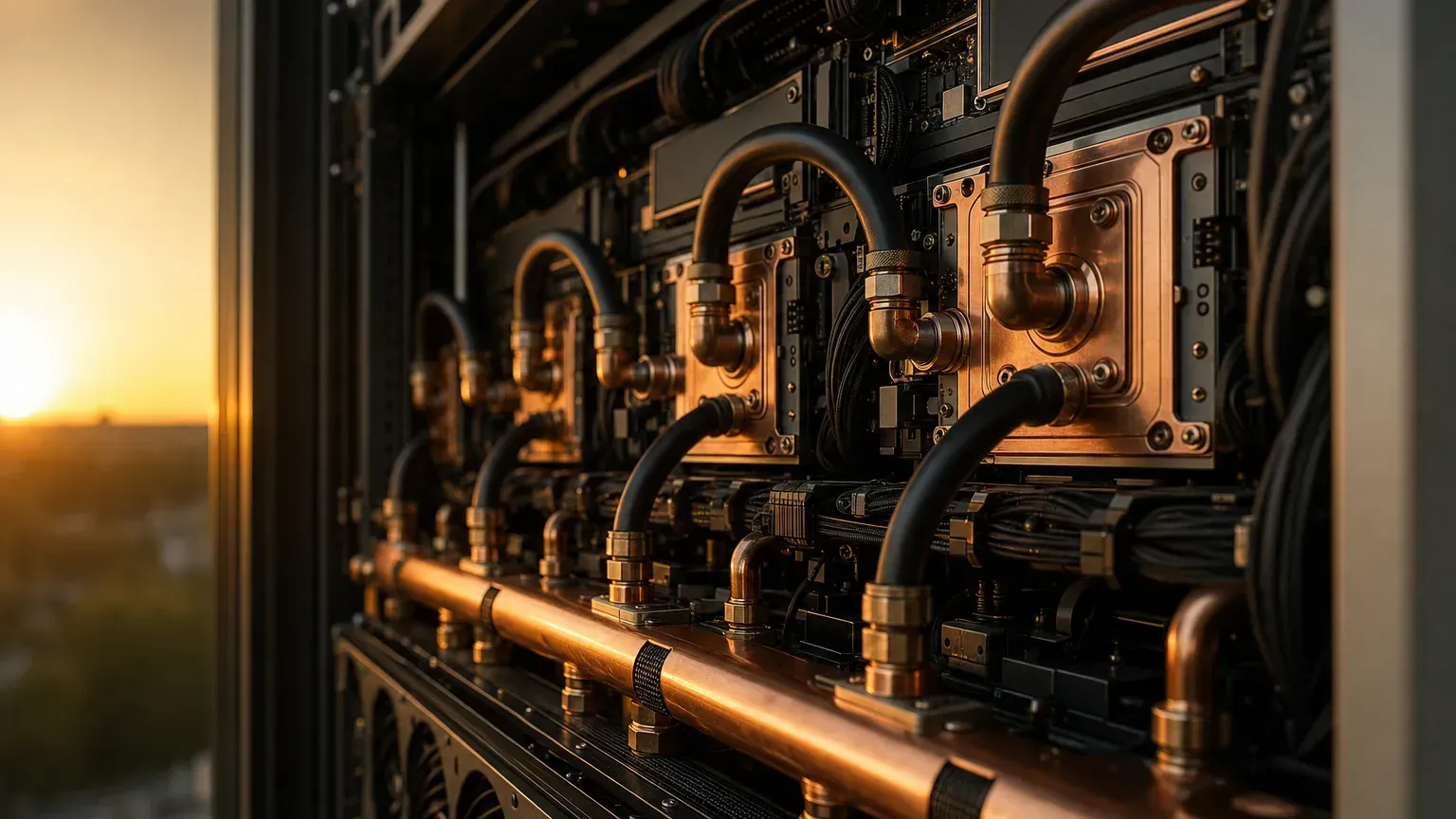

Take NVIDIA’s GB300 NVL72. A single rack integrates 72 GPUs and 36 CPUs, plus switches, power, and cooling, all bound together with liquid cooling. Pull it apart and you get roughly these layers: compute (GPU, CPU, HBM), board-level (motherboard, printed circuit board / PCB, IC substrate, connectors), interconnect (NVLink, InfiniBand, Ethernet switches), power (power supplies, busbars, backup batteries), cooling (cold plates, manifolds, quick disconnects, the cooling distribution unit / CDU), and mechanicals (rack, chassis, trays, rails, cable harnesses).

For nearly every layer, Taiwan has a representative supplier. That is exactly why a single AI server can move so many “concept stocks.”

Core-Data Snapshot

A few numbers to grasp the scale of the AI server gate. Shares and growth rates are mostly research-firm estimates.

| Topic | Data | Timing / Nature |

|---|---|---|

| 2026 global AI server shipment growth | Over 28% year-on-year | TrendForce forecast |

| Taiwan’s share of global AI server production | About 90% (production/assembly figure, not brand or revenue share) | MIC / Ministry of Economic Affairs estimate |

| GB300 NVL72 per-rack power draw | About 130-140 kilowatts | Research, 2025 H2 |

| AI data center liquid-cooling penetration | About 14% in 2024, about 33% in 2025 (still rising) | TrendForce forecast |

| ASIC-type AI server share | About 27.8% in 2026 | TrendForce forecast |

Taiwan’s Division-of-Labor Map: Seven Links

Let’s place the Taiwanese firms by link in the chain. The following are all industry-role descriptions; public information is limited, and being named does not mean orders are booked or benefits are guaranteed.

| Link | What they do | Representative Taiwanese firms |

|---|---|---|

| System / rack assembly (ODM) | Integrate GPU, CPU, power, and cooling into systems and ship full racks | Foxconn/Hon Hai, Quanta, Wistron, Wiwynn, Inventec, Gigabyte |

| Cooling / liquid cooling | Cold plates, manifolds, quick disconnects, CDU, heat spreaders | Auras, Asia Vital Components, Jentech |

| Power | Power supplies, busbars, power racks | Delta Electronics, Lite-On |

| Networking switches | Data center switches, white-box networking | Accton |

| Chassis / mechanicals | Racks, chassis, trays | Chenbro, AIC |

| Rails / connectors | Server rails, high-speed connectors, cabling | King Slide, Bizlink, Lotes, Bothhand |

| PCB / substrate | Printed circuit boards, copper-clad laminates, ABF substrates | Gold Circuit, Zhen Ding, EMC/Elite Material, Unimicron, Nan Ya PCB, Kinsus |

When NVIDIA announced platforms such as Vera, the system-manufacturing partners it listed included Taiwanese firms like Foxconn/Hon Hai, Gigabyte, Inventec, Quanta, Wistron, and Wiwynn — a sign of Taiwan’s weight at the complete-system and full-rack layer.

From GB200 to GB300: What’s Changing in the Supply Chain

A generational shift moves the supply chain’s center of gravity, and this round has three clear changes.

Liquid cooling goes from optional to standard: a GB300 NVL72 rack draws 130 to 140 kilowatts, which traditional air cooling cannot contain at all. AI data center liquid-cooling penetration is estimated to have jumped from about 14% in 2024 to about 33% in 2025, and to keep rising thereafter. That sharply raises the importance of cooling links such as cold plates, the CDU, quick disconnects, and leak detection.

Power architecture steps up: high power density forces the power architecture toward higher voltages (such as 800VDC), and power racks, busbars, and backup batteries all step up with it.

Component positions get reshuffled: as NVIDIA leans ever further toward a “full-rack integrated solution,” the ODM’s role shifts from traditional motherboard design partly toward rack-level integration, capacity, yield, and cooling/power integration. For Taiwanese firms this is both an opportunity and a margin pressure. Note that across a generational shift the BOM (bill of materials) positions change — “having a related product” is not the same as “shipping at volume.”

How to Read “AI Server Stocks”

AI servers are one of the hottest theme groups in Taiwan’s stock market, and the market puts firms from all seven links above into the discussion.

When looking at this group, what matters is understanding where each company sits in the chain and what it does. That beats memorizing a list, and it lets you quickly judge, when reading the news, “is this affecting cooling, power, or system assembly?” But remember two things. First, the often-cited “about 90% from Taiwan” is a production/assembly figure and does not mean all the profit sits with Taiwanese firms. Second, the actual customers and orders of these companies are mostly confidential, the pairings the market draws are often analyst speculation, and being named does not mean orders are booked or benefits are guaranteed. This piece only describes industry roles and division of labor; it does not compile beneficiary stocks, does not rank individual names, and does not constitute investment advice.

Key Takeaways for This Gate

After looking at AI server stocks, first fix its positioning: this is the most broadly participated and most complete segment of Taiwan’s AI supply chain, with representative firms from system and rack assembly through cooling, power, networking, mechanicals, connectors, and substrates.

As the generation moves from GB200 to GB300, liquid cooling and high-power electricity become standard, raising the weight of the cooling and power links. Understanding this division-of-labor map is useful, but remember: the map is not a stock-picking list, and being named does not mean orders are booked.

To see Taiwan’s full semiconductor division of labor, go back and read the Taiwan semiconductor supply chain; to unpack the system-assembly business model, read what ODM means and how ODM stocks are framed; to see the supply chain built specifically to serve NVIDIA, see the NVIDIA supply chain; to see why cooling is so critical, see the liquid-cooling gate; to see all eight gates of the chain, head back to the supply-chain overview.