You’ve got some USDC and you want to take it into Interactive Brokers (IBKR) to buy U.S. stocks. The traditional way: convert the USDC to dollars on an exchange, withdraw to a bank, then wire into IBKR — a conversion plus a wire, with fees and business days to count.

FluidKey offers another route: spend USDC as dollars, sent straight into the broker over ACH. Smooth as it sounds, there are plenty of fine points worth spelling out.

How the route works

FluidKey connects to the fiat rails through Bridge (the payments infrastructure Stripe acquired; the entity is Bridge Building Limited). You deposit USDC into FluidKey, it sits there as dollars, and then it’s sent into IBKR over ACH. IBKR’s ACH deposit gives you receiving details tied to your account, with UMB Bank, National Association as the receiving bank.

In one line: USDC → (FluidKey converts to USD via Bridge) → ACH → your dedicated account at IBKR.

The actual steps

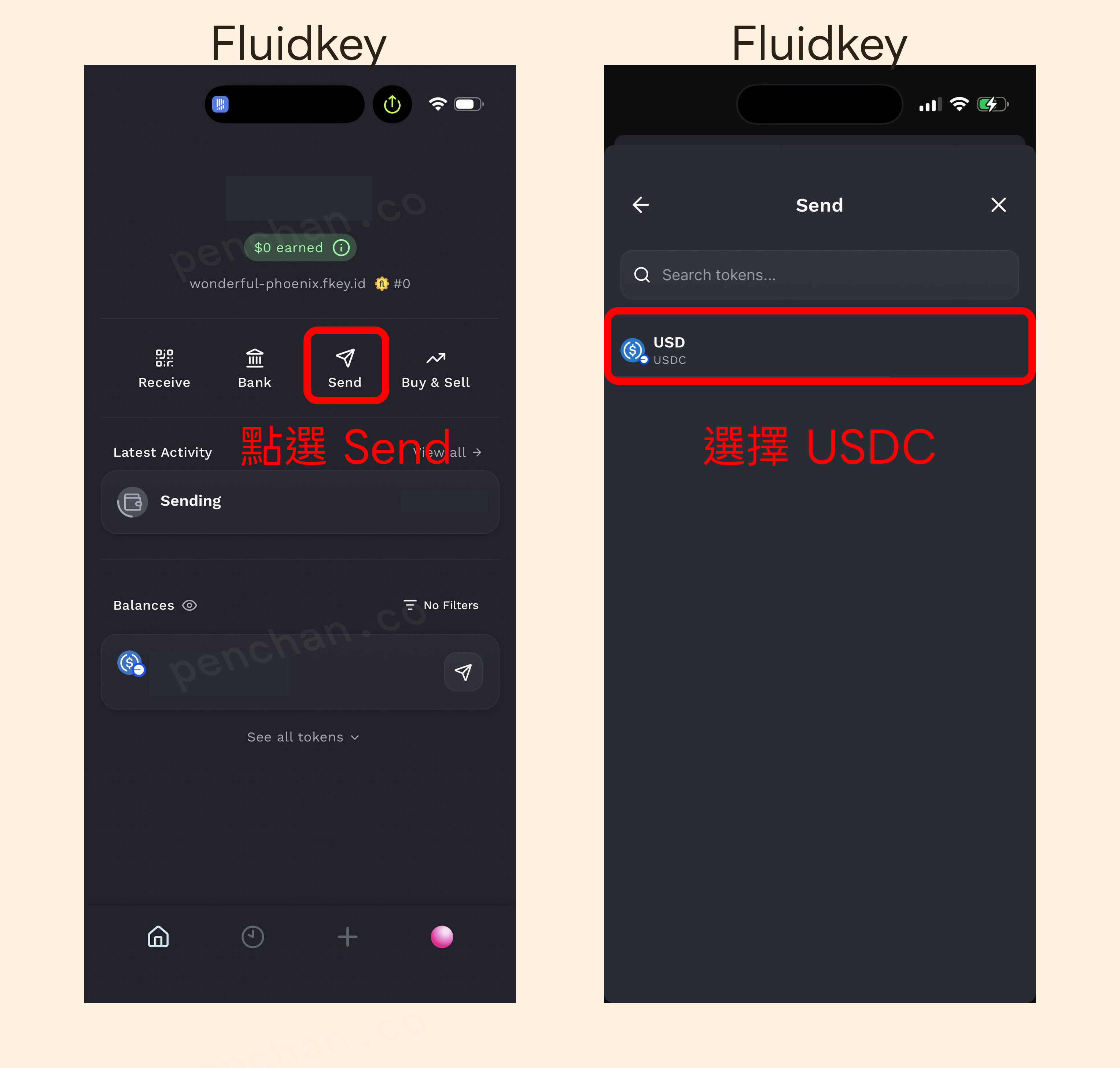

Step 1: Start a USD transfer in FluidKey

In FluidKey, after depositing USDC, tap Send and choose USD (USDC). On the Send USDC screen, tap the bank icon next to the address field and open Add Bank Account.

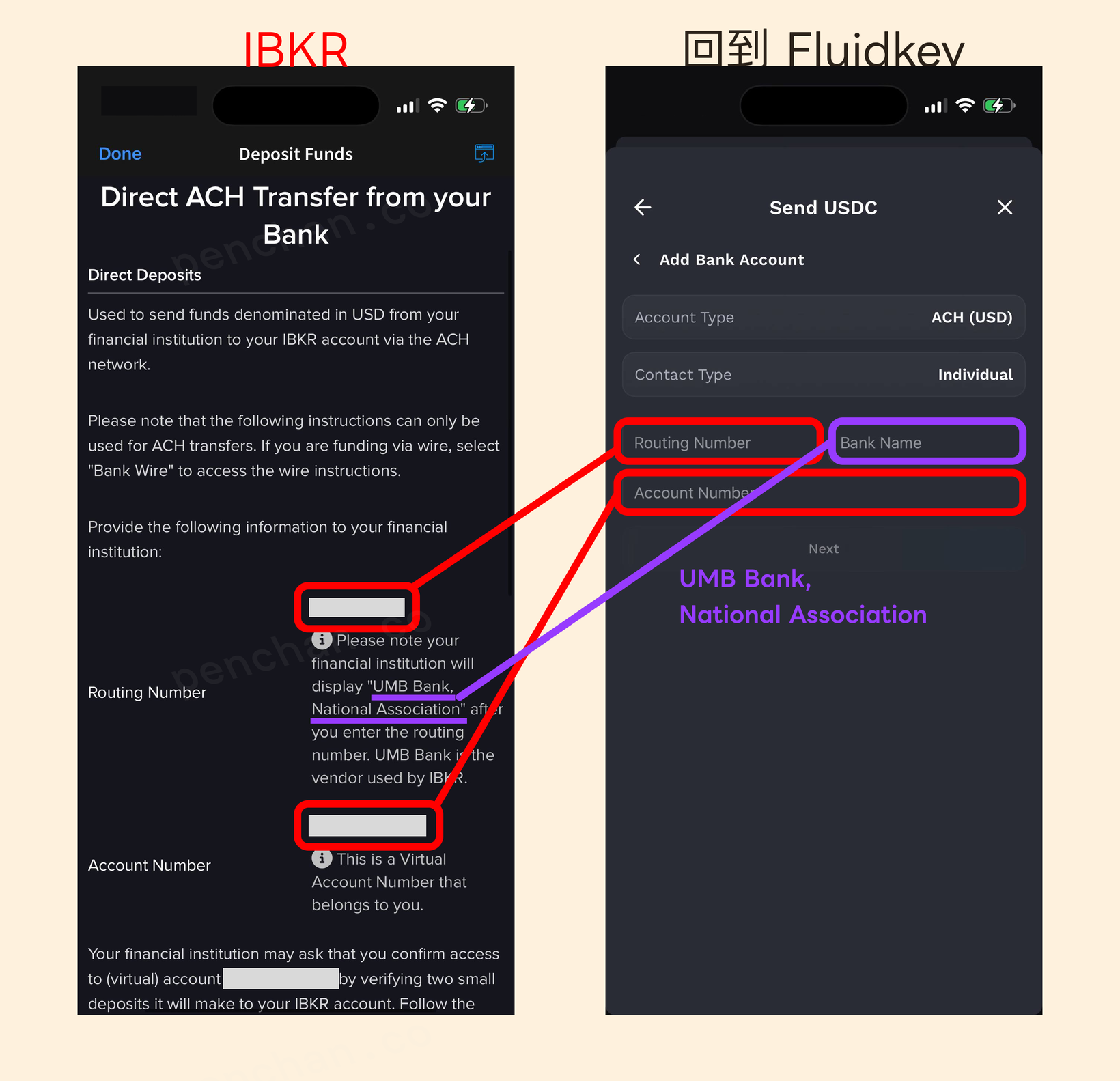

Set Account Type to ACH (USD) and Contact Type to Individual. Leave the Routing Number, Bank Name, and Account Number blank for now — you’ll get those from IBKR.

Step 2: Get the ACH deposit details from IBKR

In IBKR, go to Deposit Funds, choose USD, and pick Direct ACH Transfer from your Bank (officially about 1 business day).

IBKR gives you a Routing Number and a dedicated Account Number tied to your account, with UMB Bank, National Association as the receiving bank.

Step 3: Fill it back into FluidKey and send

Back in the Add Bank Account form, fill the three fields with what IBKR gave you: paste the Routing Number and Account Number, and set Bank Name to UMB Bank, National Association. Confirm the amount and send.

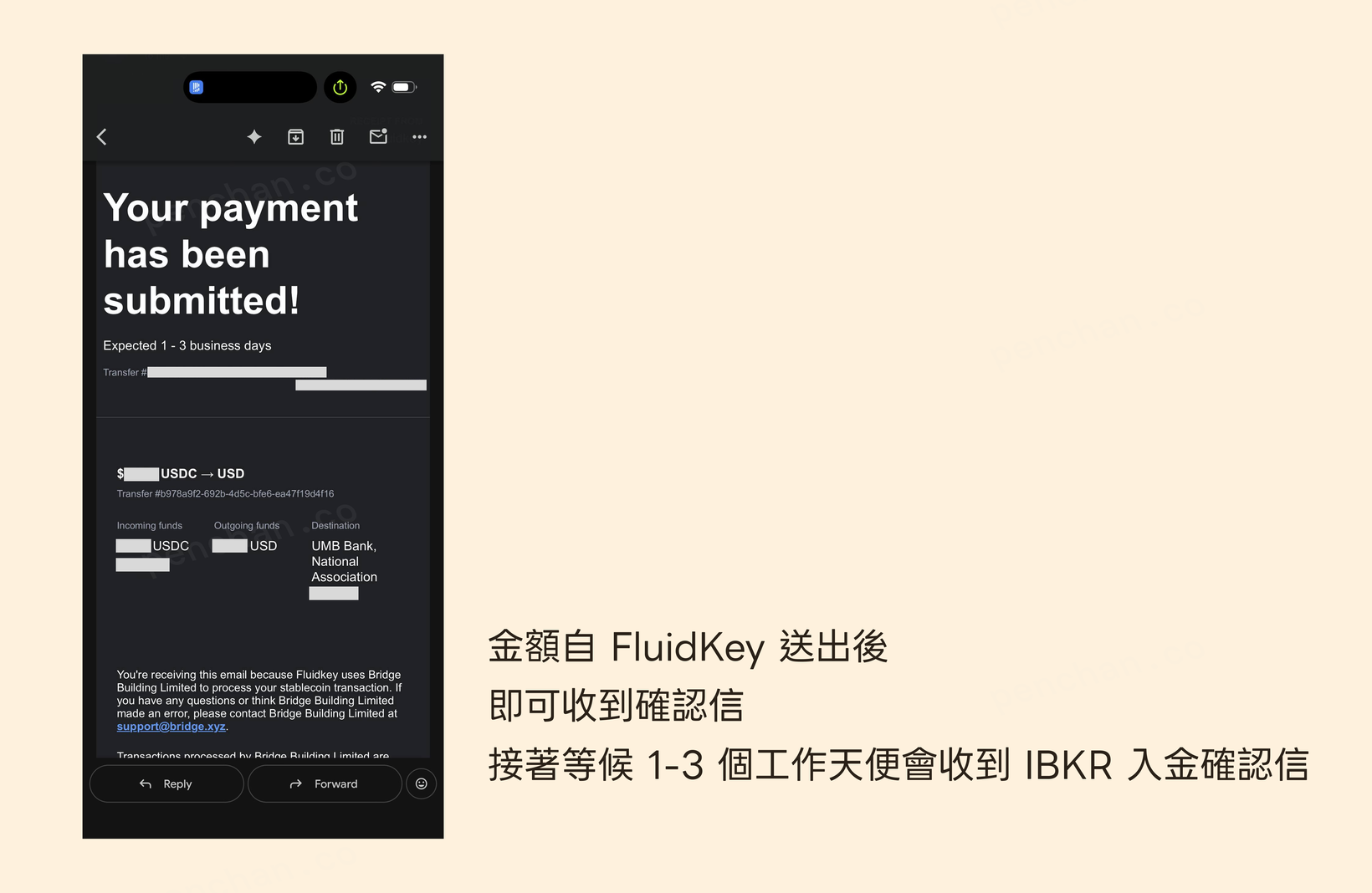

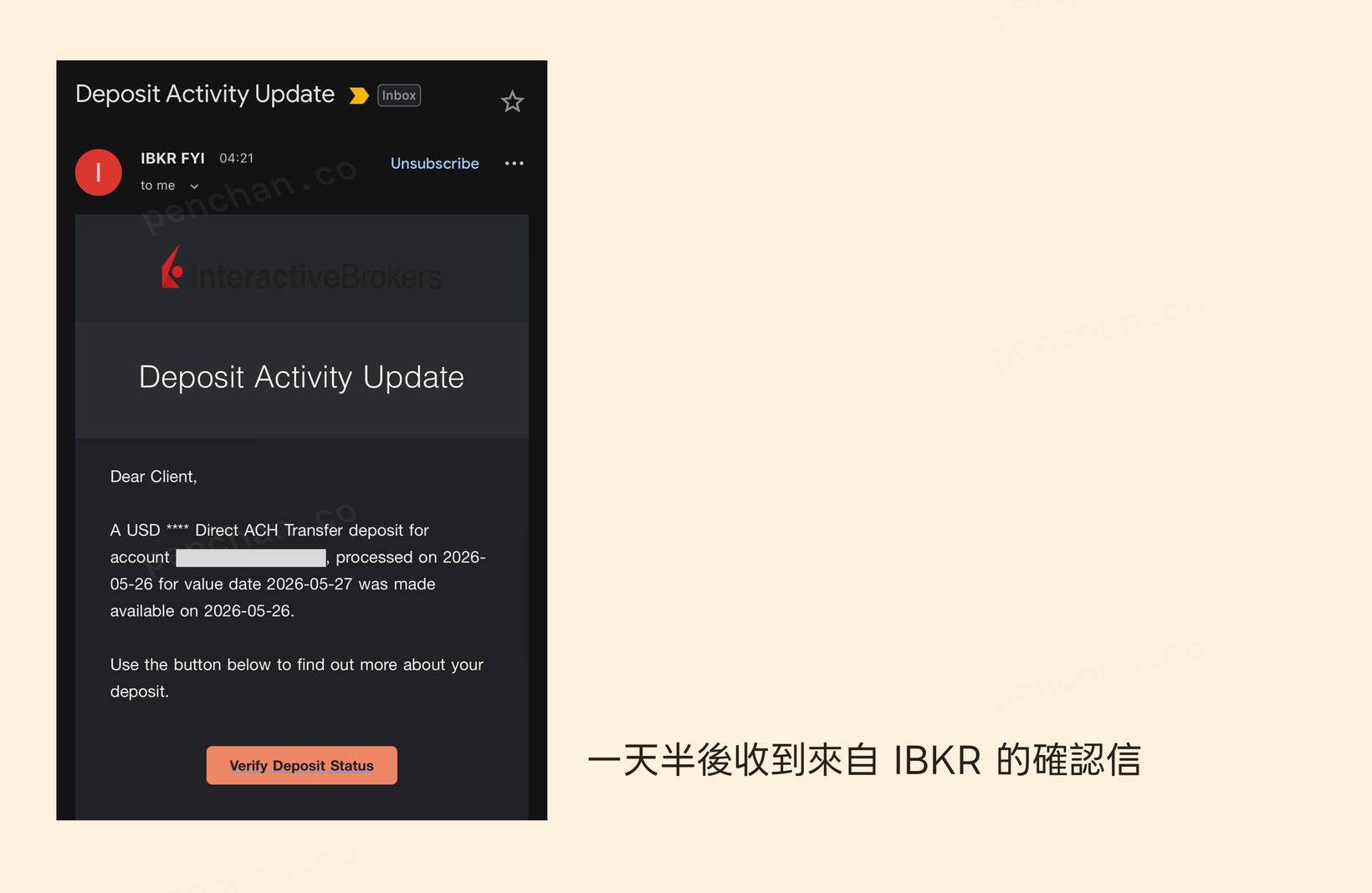

Step 4: Wait for the confirmation, 1–3 business days to land

Right after you send, you get a confirmation email (from Bridge Building Limited) showing USDC → USD, destination UMB Bank, estimated 1 to 3 business days. Once the funds land in IBKR, you’ll get IBKR’s own deposit confirmation, and the route is complete.

One real test took about a day and a half: sent from FluidKey on the afternoon of 5/25, IBKR’s deposit-confirmation email arrived early on 5/27 — within the “1 to 3 business days” window.

Risks and red lines

Names have to match. IBKR rejects third-party deposits across all three of its main entities (LLC/HK/SG). This route works because IBKR’s ACH deposit uses a dedicated Account Number tied to your own account, and FluidKey is KYC’d in your name too. If the names don’t match, it gets bounced.

Regional eligibility. FluidKey’s bank-account feature is provided through Bridge; whether it opens for residents of a given region, and the limits, vary — you have to actually apply and see. Don’t assume it works until you’ve tested it through. (Strongly recommend testing with ~10 USDC before going big.)

Foreign exchange and reporting. Individuals have annual foreign-exchange allowances and reporting rules; large transfers can trigger AML review, where you must account for the source of funds (SoF). A privacy tool only reduces on-chain linkage — reporting and tax still apply.

One more processor in the chain. The funds are actually handled and converted by Bridge, a third party beyond FluidKey. If something goes wrong, the contact point may be Bridge (the email includes a support address), so the chain of responsibility is one link longer than a direct wire.

Amount guidance. Better suited to small amounts or testing. For large sums, compliance review and cost scale up (the first tier charges a fee above 3,000 USD; check the current official numbers), and many people find a same-name bank wire more reliable.

Self-custody and offshore. Lose your keys and no one can save you; not supervised by Taiwan’s FSC and not covered by deposit insurance.

Invite links and a reminder

This route uses two services, so the links are here for easy sign-up: FluidKey (stablecoin wallet) and IBKR (broker). Both are referral links; signing up through them earns Penchan a referral reward and doesn’t affect your fees.

If you want to run the flow in reverse and pull money from IBKR back into USDC, see the withdrawal test.

The first time, definitely run a small, won’t-miss-it amount through the whole route, confirm the same-name match and that it lands, then scale up.

FAQ

How much does FluidKey charge? New users (Fluidkey Score under 10K) get $3,000 of free allowance per month (deposits and withdrawals combined); above that it’s 0.3%. Higher tiers and the latest rates are on the official site: https://docs.fluidkey.com/readme/bank

Is funding IBKR with stablecoins legal? Converting USDC you legally hold into dollars and sending it to a brokerage account in your own name isn’t illegal in itself. The conditions: a clear source of funds, reporting per the rules, and paying tax. Using a privacy tool to dodge reporting is the real risk.

Will it always work? No guarantee. IBKR’s ACH deposit uses a dedicated Account Number tied to your own account, so the account must match by name; whether FluidKey’s bank feature opens for your region also needs testing. Test small first.

Why not just wire? If you already hold USDC, it skips the conversion and some intermediaries, with ACH from $1. The trade-off is it suits small amounts or testing.

How long to land? You get Bridge’s confirmation right after sending; the funds land in IBKR in about 1 to 3 business days, varying with conditions at the time.

The most appealing thing about this route (fast, smooth, USDC spending like dollars) is also the easiest place to forget about compliance — like forgetting the old hassle of wiring: trekking to the bank, filling out forms. The technical part is done in four steps; the real variable is whether residents of Taiwan or other regions clear KYC. There are already cases that have run through end to end (including this article’s timing test), but one success doesn’t mean it works for everyone — here’s wishing you a smooth path to the stocks you’re after.